Unit 1: Supply

Supply: The quantity that producers or sellers are willing and able to produce or sell at various prices

The Law of Supply: There is a direct relationship between price and quantity supplied (as price increases, so does quantity).

- A change in price causes a change in quantity supplied.

(Supply curves are always upward sloping.)

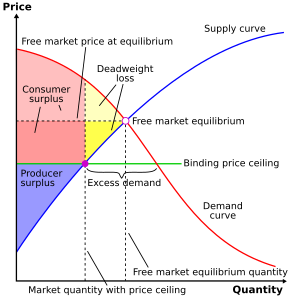

Price Ceiling: Legal maximum price meant to help buyers

-Ex: Rent control

4 Consequences for low set price ceiling:

Price Floor: Legal minimum price meant to help sellers keep product prices from falling

-Ex: Minimum wage

4 Consequences of price floor:

The Law of Supply: There is a direct relationship between price and quantity supplied (as price increases, so does quantity).

- A change in price causes a change in quantity supplied.

(Supply curves are always upward sloping.)

Causes of "Change in supply":

- ▲in the number of seller

- ▲in the cost of production

- ▲in technology

- ▲in weather

- ▲in taxes and subsidies (money the government provides)

Fixed price: Cost that does not change no matter how much of a good is being produced.

-Ex: Salary, mortgage, and insurance

Variable cost: Cost that rises or falls depends upon how much is provided.

-Ex: Electricity

Marginal cost: cost of producing on more unit of a good

Revenue: Receiving

-Ex: Income

Cost: Spending (goes out).

Formulas:

(Key: Q-quantity, TFC- total fixed cost, TVC- total variable cost, TC- total cost, MC- marginal cost, AFC- average fixed cost, AVC- average variable cost, ATC- average total cast.)

- TFC=ATC X Q

- TVC=AVC X Q

- TC= ATC X Q

- TFC + TVC= TC

- AFC+ AVC= ATC

- TFC/Q=AFC

- TVC/Q=AVC

- TC/Q=ATC

Price Ceiling: Legal maximum price meant to help buyers

-Ex: Rent control

4 Consequences for low set price ceiling:

- Lower prices for some consumers

- Shortages

- Long lines for some buyers

- Illegal sales above the equilibrium price

Price Floor: Legal minimum price meant to help sellers keep product prices from falling

-Ex: Minimum wage

4 Consequences of price floor:

- Higher product prices

- Surplus

- Higher taxes

- Waste

-Business cycle: Fluctuation in economic activity that an economy experiences over a period of time.

-Expansion: A period of economic upturn, when output and employment are rising.

-Peak: Where business activity has reached a temporary maximum. Near, or at, full employment.

-Contraction: Better known as a recession. A period of decline in total output, income, and employment

-Trough: Lowest point. Point in which the economy turns from recession to depression.

Very informational notes but you should explain the shifts of supply curve and what they mean.

ReplyDeleteThis post was very helpful but I just wanted to elaborate on Surplus which is an amount of something left over when requirements have been met; an excess of production or supply over demand.

ReplyDelete